See Starting a Business data here.

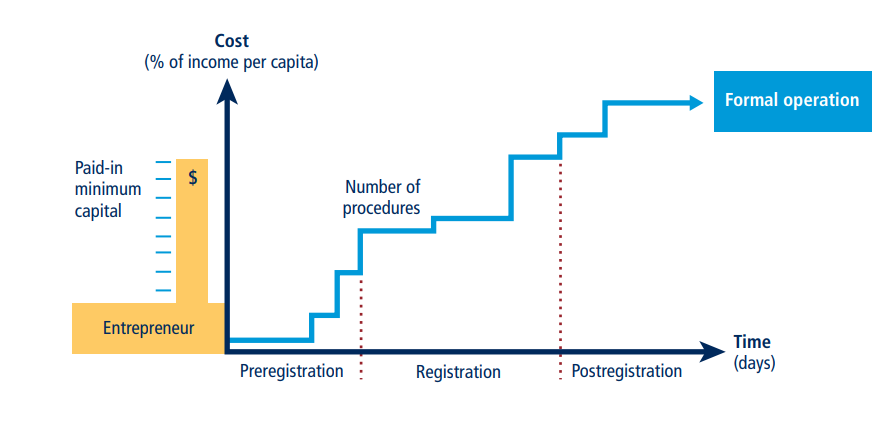

Doing Business records all procedures officially required, or commonly done in practice, for an entrepreneur to start up and formally operate an industrial or commercial business, as well as the time and cost to complete these procedures and the paid-in minimum capital requirement (figure 1). These procedures include the processes entrepreneurs undergo when obtaining all necessary approvals, licenses, permits and completing any required notifications, verifications or inscriptions for the company and employees with relevant authorities. The ranking of economies on the ease of starting a business is determined by sorting their scores for starting a business. These scores are the simple average of the scores for each of the component indicators.

Two types of local limited liability companies are considered under the starting a business methodology. They are identical in all aspects, except that one company is owned by five married women and other by five married men. The score for each indicator is the average of the scores obtained for each of the component indicators for both of these standardized companies.

After a study of laws, regulations and publicly available information on business entry, a detailed list of procedures is developed, along with the time and cost to comply with each procedure under normal circumstances and the paid-in minimum capital requirement. Subsequently, local incorporation lawyers, notaries and government officials review and verify the data.

Information is also collected on the sequence in which procedures are to be completed and whether procedures may be carried out simultaneously. It is assumed that any required information is readily available and that the entrepreneur will pay no bribes. If answers by local experts differ, inquiries continue until the data are reconciled.

To make the data comparable across economies, several assumptions about the businesses and the procedures are used.

Assumptions about the business

The business:

- Is a limited liability company (or its legal equivalent). If there is more than one type of limited liability company in the economy, the limited liability form most common among domestic firms is chosen. Information on the most common form is obtained from incorporation lawyers or the statistical office.

- Operates in the economy’s largest business city. For 11 economies the data are also collected for the second largest business city.

- Performs general industrial or commercial activities, such as the production or sale to the public of goods or services. The business does not perform foreign trade activities and does not handle products subject to a special tax regime, for example, liquor or tobacco. It is not using heavily polluting production processes.

- Does not qualify for investment incentives or any special benefits.

- Is 100% domestically owned

- Has five business owners, none of whom is a legal entity. One business owner holds 30% of the company shares, two owners have 20% of shares each, and two owners have 15% of shares each.

- Is managed by one local director.

- Has between 10 and 50 employees one month after the commencement of operations, all of them domestic nationals.

- Has start-up capital of 10 times income per capita.

- Has an estimated turnover of at least 100 times income per capita.

- Leases the commercial plant or offices and is not a proprietor of real estate.

- Has an annual lease for the office space equivalent to one income per capita.

- Is in an office space of approximately 929 square meters (10,000 square feet).

- Has a company deed that is 10 pages long.

The owners:

- Have reached the legal age of majority and are capable of making decisions as an adult. If there is no legal age of majority, they are assumed to be 30 years old.

- Are sane, competent, in good health and have no criminal record.

- Are married, the marriage is monogamous and registered with the authorities.

- Where the answer differs according to the legal system applicable to the woman or man in question (as may be the case in economies where there is legal plurality), the answer used will be the one that applies to the majority of the population.

Procedures

A procedure is defined as any interaction of the company founders with external parties (for example, government agencies, lawyers, auditors or notaries) or spouses (if legally required). Interactions between company founders or company officers and employees are not counted as procedures. Procedures that must be completed in the same building but in different offices or at different counters are counted as separate procedures. If founders have to visit the same office several times for different sequential procedures, each is counted separately. The founders are assumed to complete all procedures themselves, without middlemen, facilitators, accountants or lawyers, unless the use of such a third party is mandated by law or solicited by the majority of entrepreneurs. If the services of professionals are required, procedures conducted by such professionals on behalf of the company are counted as separate procedures. Each electronic procedure is counted as a separate procedure. Approvals from spouses to own a business or leave the home are considered procedures if required by law or if by failing to obtain such approval the spouse will suffer consequences under the law, such as the loss of right to financial maintenance. Obtaining permissions only required by one gender for company registration and operation, or getting additional documents only required by one gender for a national identification card are considered additional procedures. In that case, only procedures required for one spouse but not the other are counted. Both pre- and post-incorporation procedures that are officially required or commonly done in practice for an entrepreneur to formally operate a business are recorded.

Procedures required for official correspondence or transactions with public agencies are also included. For example, if a company seal or stamp is required on official documents, such as tax declarations, obtaining the seal or stamp is counted. Similarly, if a company must open a bank account in order to complete any subsequent procedure—such as registering for value added tax or showing proof of minimum capital deposit—this transaction is included as a procedure. Shortcuts are counted only if they fulfill four criteria: they are legal, they are available to the general public, they are used by the majority of companies, and avoiding them causes delays.

Only procedures required for all businesses are included. Industry-specific procedures are excluded. For example, procedures to comply with environmental regulations are included only when they apply to all businesses conducting general commercial or industrial activities. Procedures that the company undergoes to connect to electricity, water, gas and waste disposal services are not included in the starting a business indicators.

Time

Time is recorded in calendar days. The measure captures the median duration that incorporation lawyers or notaries indicate is necessary in practice to complete a procedure with minimum follow-up with government agencies and no unofficial payments. It is assumed that the minimum time required for each procedure is one day, except for procedures that can be fully completed online, for which the minimum time required is recorded as half a day. Although procedures may take place simultaneously, they cannot start on the same day (that is, simultaneous procedures start on consecutive days). A registration process is considered completed once the company has received the final incorporation document or can officially commence business operations. If a procedure can be accelerated legally for an additional cost, the fastest procedure is chosen if that option is more beneficial to the economy’s score. When obtaining a spouse’s approval, it is assumed that permission is granted at no additional cost unless the permission needs to be notarized. It is assumed that the entrepreneur does not waste time and commits to completing each remaining procedure without delay. The time spent by the entrepreneur preparing information to fill in forms is not measured. It is assumed that the entrepreneur is aware of all entry requirements and their sequence from the beginning but has had no prior contact with any of the officials involved.

Cost

Cost is recorded as a percentage of the economy’s income per capita. It includes all official fees and fees for legal or professional services if such services are required by law or commonly used in practice. Fees for purchasing and legalizing company books are included if these transactions are required by law. Although value added tax registration can be counted as a separate procedure, value added tax is not part of the incorporation cost. The company law, the commercial code and specific regulations and fee schedules are used as sources for calculating costs. In the absence of fee schedules, a government officer’s estimate is taken as an official source. In the absence of a government officer’s estimate, estimates by incorporation experts are used. If several incorporation experts provide different estimates, the median reported value is applied. In all cases the cost excludes bribes.

Paid-in minimum capital

The paid-in minimum capital requirement reflects the amount that the entrepreneur needs to deposit in a bank or with a third-party (for example, a notary) before registration or up to three months after incorporation and it is recorded as a percentage of the economy’s income per capita. The amount is typically specified in the commercial code or the company law. The legal provision needs to be adopted, enforced and fully implemented. Any legal limitation of the company’s operations or decisions related to the payment of the minimum capital requirement is recorded. In case the legal minimum capital is provided per share, it is multiplied by the number of shareholders owning the company. Many economies require minimum capital but allow businesses to pay only a part of it before registration, with the rest to be paid after the first year of operation. In El Salvador in May 2019, for example, the minimum capital requirement was $2,000, of which 5% needed to be paid before registration. Therefore, the paid-in minimum capital recorded for El Salvador is $100, or 2.6% of income per capita.

Reforms

The starting a business indicator set tracks changes related to the ease of incorporating and operating a limited liability company every year. Depending on the impact on the data, certain changes are classified as reforms and listed in the summaries of Doing Business reforms in order to acknowledge the implementation of significant changes. Reforms are divided into two types: those that make it easier to do business and those changes that make it more difficult to do business. The starting a business indicator set uses one criterion to recognize a reform.

The impact of data changes is assessed based on the absolute change in the overall score of the indicator set as well as the change in the relative score gap. Any data update that leads to a change of 0.5 points or more in the score and 2% or more on the relative score gap is classified as a reform, except when the change is the result of automatic official fee indexation to a price or wage index (for more details, see the chapter on the ease of doing business score and ease of doing business ranking). For example, if the implementation of a new one-stop shop for company registration reduces time and procedures in a way that the score increases by 0.5 points or more and the overall gap decreases by 2% or more, the change is classified as a reform. Minor fee updates or other small changes in the indicators that have an aggregate impact of less than 0.5 points on the overall score or 2% on the gap are not classified as a reform, but the data are updated accordingly.

This methodology was developed by Djankov and others (2002) and is adopted here with minor changes.